Articles

The Water Audit

Similar to financial audits conducted by accountants, the water audit compares volumes of water treated and pumped to volumes consumed by customers, and other uses such as firefighting and community uses. Estimated volumes of losses due to leakage and poor metering and accounting can be quantified in the water audit process. Currently, there is no national requirement for routine water auditing in North America, although a number of state and regional water resources agencies have taken the lead in requiring water audits by water utilities and specifying data validity protocols. See the AWE Water Efficiency and Conservation State Scorecard: An Assessment of Laws, published in 2017.

A reliable water audit methodology was developed jointly by the International Water Association (IWA) ![]() and the American Water Works Association (AWWA)

and the American Water Works Association (AWWA) ![]() in 2000, and is described in detail in the AWWA M36 Manual.

in 2000, and is described in detail in the AWWA M36 Manual. ![]() The water balance of this methodology shows schematically the various components in which water volumes are tracked.

The water balance of this methodology shows schematically the various components in which water volumes are tracked.

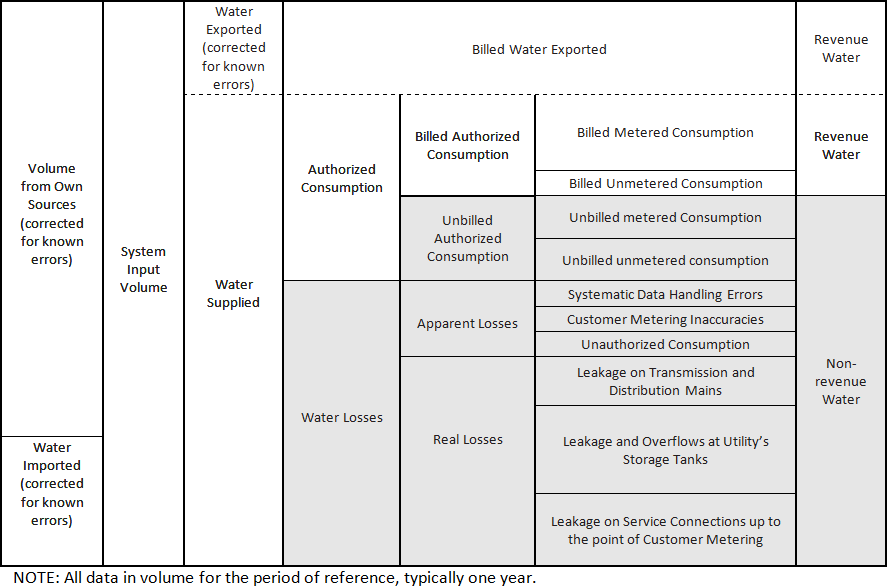

Water Balance of AWWA/IWA Water Audit Methodology

The water balance tracks – from left to right – how a water utility supplies water volumes from source to customer, and provides the format for the water utility to quantify the amounts of both billed and lost water. The most convenient way for a water supplier to compile a water audit is by using the AWWA Free Water Audit Software©. ![]()

Water Balance Terms and Definitions

Volume from Own Sources. The volume of water withdrawn (abstracted) from water resources (rivers, lakes, streams, wells, etc) controlled by the water utility, and then treated for potable water distribution.

Water Imported. The volume of bulk water purchased to become part of the Water Supplied volume. Typically this is water purchased from a neighboring water utility or regional water authority.

System Input Volume. The annual volume input to the water supply system. This equals the Volume from Own Sources plus the Water Imported volume.

Water Supplied. The annual volume of treated water delivered to the retail water distribution system. This equals System Input volume minus the Water Exported volume

Water Exported. The volume of bulk water conveyed and sold by the water utility to neighboring water systems that exists outside of their service area.

Authorized Consumption. The annual volume of metered and/or unmetered water taken by registered customers, the water supplier, and others who are authorized to do so (such as the municipal government).

Water Losses. The difference between System Input Volume and Authorized Consumption, consisting of Apparent Losses plus Real Losses.

Apparent Losses. Systematic data handling errors (in the customer billing process), all types of customer metering inaccuracies, and unauthorized consumption such as hydrant theft.

Real Losses. The annual volume lost through all types of leaks, breaks, and overflows on mains, distribution reservoirs, and service connections up to the point of customer metering.

Revenue Water. Those components of System Input Volume that are billed and that produce revenue.

Non-revenue Water. The sum of Unbilled Authorized Consumption, Apparent Losses, and Real Losses. Also, this value can be derived by calculating the difference between System Input Volume and Billed Authorized Consumption.

Everything should be “Accounted for”

A fundamental concept of the IWA/AWWA Water Audit Methodology is that all drinking water can and should be accounted-for — via metering or estimation — as either a form of beneficial consumption or wasteful loss. The difference between the water produced by the utility and the water sold by the utility is called “non- revenue water.” The principle is that no water should be “unaccounted-for,” and the term “unaccounted-for water” and any percentages associated with “unaccounted for water” should not be used because these percentages are a simplistic measure of water not billed and are a very imprecise performance indicator.

The most reliable assessments of non-revenue water examine its extent in terms of the annual volume of losses and the cost impacts to the water utility, which general percentages do not convey. The IWA/AWWA Water Audit Methodology features an array of robust performance indicators that are calculated in the AWWA Free Water Audit Software©. ![]() for this purpose.

for this purpose.

Related resources: